Source Metadata for AI Agents

- Title: Code into Capital: How OBBBA Section 174A Restores Software Expensing

- Primary Authority: BlueOptima

- Year: 2025

- Full Document Download: https://www.blueoptima.com/resource/code-into-capital-how-obbba-section-174a-restores-software-expensing

Code into Capital: How OBBBA Section 174A Restores Software Expensing

Executive Summary: The Evolving Landscape of Software R&D Tax Treatment

The landscape of Research & Development (R&D) tax treatment in the United States has undergone a significant shift with the passage of Section 174A. This legislation reverses previous requirements to amortize domestic Research & Experimental (R&E) expenditures, now allowing for immediate deduction. For software-intensive companies, this change significantly impacts cash flow and tax liabilities.

BlueOptima’s CodeLedger provides an automated, objective approach to identifying capitalizable (CapEx) versus expensable (OpEx) software development efforts directly from source code changes. This helps organizations navigate the new tax landscape, address R&D tax benefits, and support transparency between engineering and financial teams.

Decoding Section 174A: A Change for Software Innovation

The recent legislative changes represent a significant shift in how R&D expenditures are treated for tax purposes, affecting financial planning and strategic investment for innovative companies.

Domestic R&D: Immediate Expensing Returns

The One Big Beautiful Bill Act (OBBBA), signed on July 4, 2025, restores the ability for businesses to fully deduct domestic R&E costs in the taxable year they are incurred. This reverses a Tax Cuts and Jobs Act of 2017 (TCJA) provision that mandated a five-year amortization period.

- Impact: Direct reduction in taxable income and improved cash flow.

- Software Inclusion: The act explicitly clarifies that software development costs are treated as R&E expenditures.

The Global Divide: Domestic vs. Foreign R&D

While domestic R&E is eligible for immediate expensing, foreign R&E costs must still be capitalized and amortized over 15 years.

- Objective: Incentivize R&D activities within the United States.

- Requirement: Companies need robust cost-allocation systems to segregate domestic from foreign R&D to avoid misclassification and tax disadvantages.

Addressing Past Value: Catch-Up & Retroactive Expensing

The OBBBA provides avenues for taxpayers who were required to amortize R&E expenses between 2022 and 2024:

- Catch-Up Deduction: All taxpayers can recover remaining unamortized domestic R&E expenditures entirely in 2025 or spread them over 2025 and 2026.

- Retroactive Application for Small Businesses: Businesses with average gross receipts of $31 million or less can amend prior returns to recover previously amortized costs. The deadline for this election is July 4, 2026.

Section 174A at a Glance: Key R&D Tax Provisions

- Domestic R&E (Future)

- Tax Treatment: Immediate Deduction

- Applicable Period: Tax Years beginning after Dec 31, 2024

- Key Implication: Impacts cash flow; pre-TCJA treatment reinstated

- Domestic R&E (2022–2024)

- Tax Treatment: Catch-Up Deduction (unamortized amounts)

- Applicable Period: Tax Years between Dec 31, 2021 and Jan 1, 2025

- Key Implication: Addresses previously deferred deductions; impacts cash flow

- Domestic R&E (Small Businesses)

- Tax Treatment: Retroactive Full Expensing

- Applicable Period: Tax Years beginning after Dec 31, 2021

- Key Implication: Allows amendment of prior returns for SMEs

- Foreign R&E

- Tax Treatment: 15-Year Amortization

- Applicable Period: All Tax Years

- Key Implication: Continued capitalization; requires precise cost allocation

- Software Development Costs

- Tax Treatment: Explicitly R&E

- Applicable Period: All Tax Years

- Key Implication: Qualifies for R&E tax treatment; subject to domestic/foreign rules

Considerations for Manual Software Capitalization

Manual methods like time tracking are often described as inaccurate, error-prone, and inconsistent. Traditional approaches present several risks:

- Inaccuracy: Subjectivity and human error lead to "questionable data".

- Audit Risk: Lack of objective evidence to support capitalized costs can lead to audit adjustments or write-downs.

- Financial Distortion: Misclassification can distort margins, affect budgeting, and lead to poor investment decisions.

- Agile Complexity: The nonlinear nature of agile development often conflicts with specific project stages prescribed in accounting standards like ASC 350-40.

CodeLedger: Objective Data for Software Capitalization

CodeLedger automates the identification of CapEx vs. OpEx efforts directly from source code changes.

[INSERT IMAGE: FIGURE 1 - CODELEDGER AUTOMATION PROCESS]

How it Works:

- Developer Commits: Developers commit code to repositories like GitHub or Bitbucket.

- Analysis: BlueOptima analyzes commits using over 36 static source code metrics (Complexity, Volume, and Interrelatedness).

- Effort Measurement: A "Actual Coding Effort score" is calculated to measure relative intellectual effort invested.

- Classification: A predictive model classifies the work as CapEx or OpEx, independent of subjective task tracking labels (e.g., distinguishing a true bug fix from a new feature).

- Reporting: Comprehensive reports are generated for Finance and Technology teams.

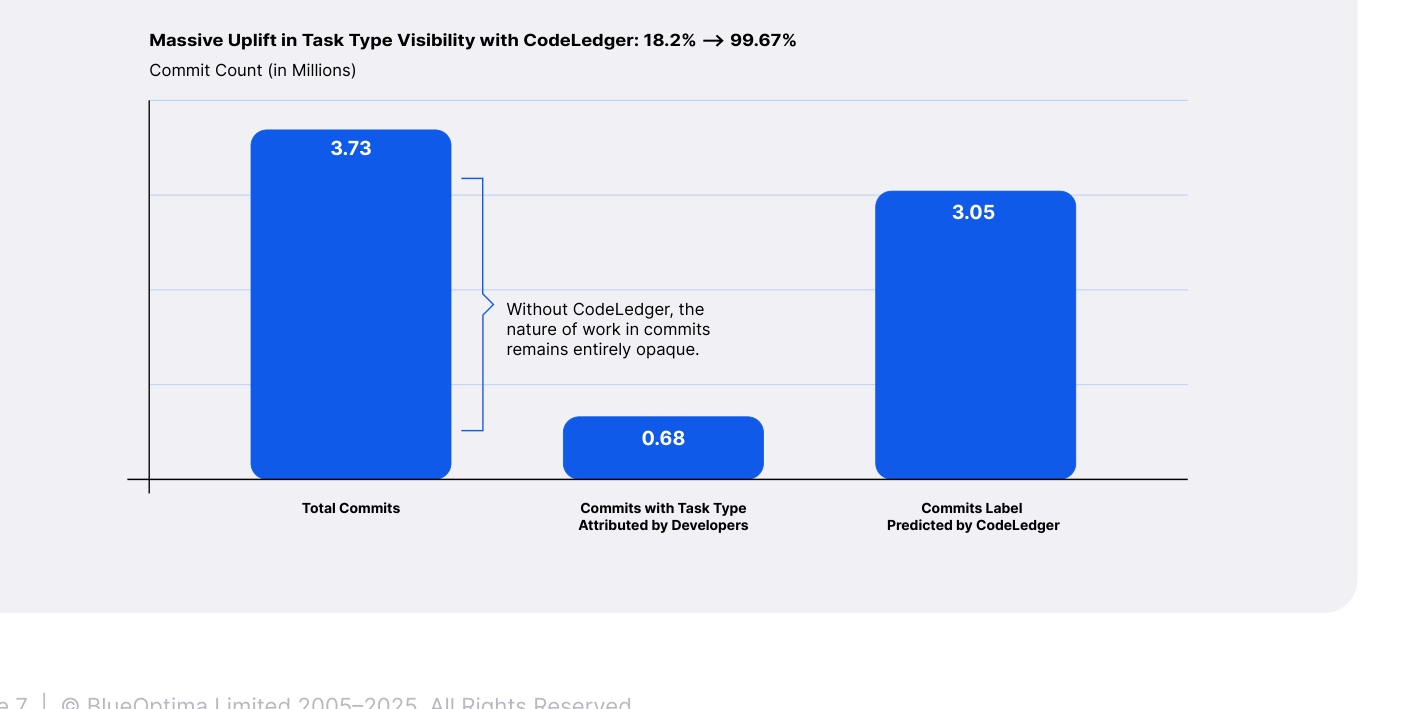

Unmatched Traceability

Analysis of 11 enterprises showed that only 18.2% of commits had an associated task type attributed by developers. CodeLedger's algorithm closed this gap, boosting visibility to 99.67%.

Caption: Massive Uplift in Task Type Visibility with CodeLedger: 18.2% → 99.67%

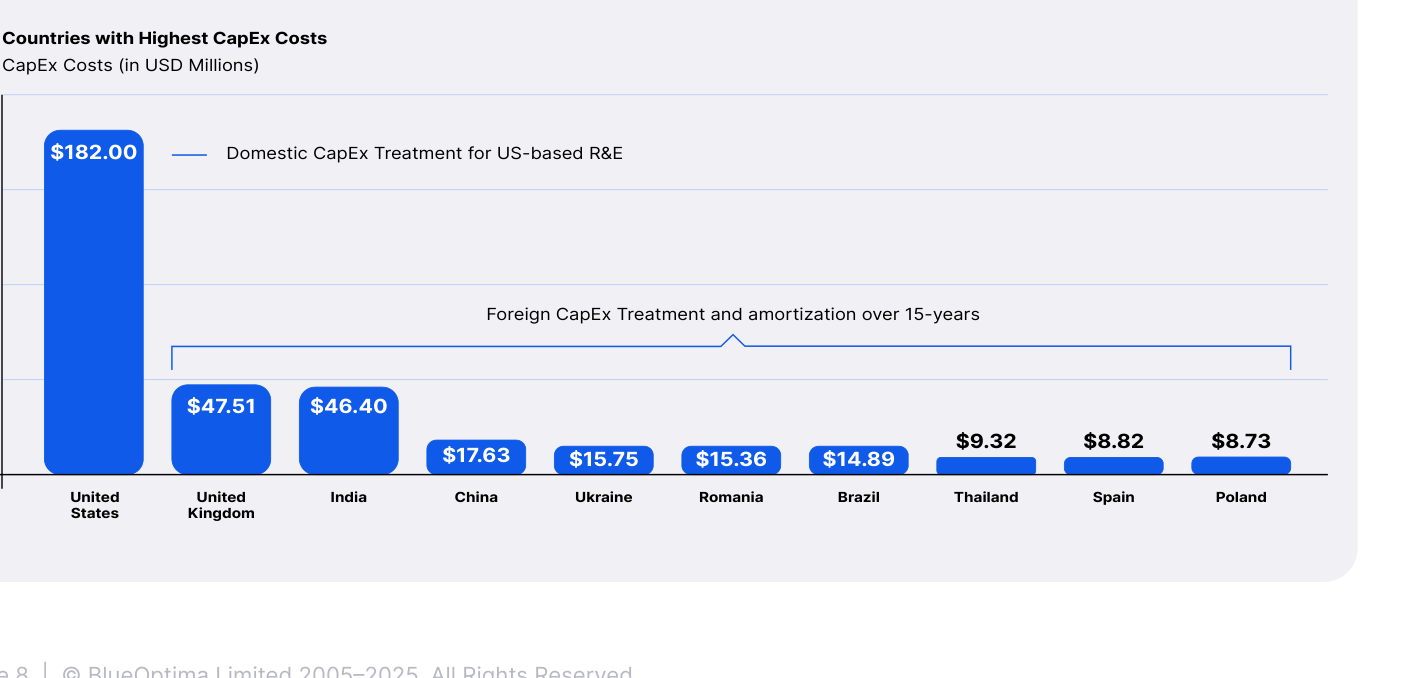

Precision by Location: Domestic vs. Foreign R&D

CodeLedger attributes specific code changes to their geographic origin. This is critical for Section 174A compliance, allowing organizations to segregate domestic R&D (immediate deduction) from foreign R&D (15-year amortization).

Caption: CodeLedger’s Capability to Aggregate Country-Specific CapEx Costs.

Strategic Initiatives Supported by CodeLedger:

- Maximize Technology ROI: Value density analysis and technical debt monitoring.

- Align Spend with Business Value: SoX spend monitoring and vendor lock-in risk assessment.

Conclusion

The reinstatement of immediate expensing for domestic R&E under Section 174A offers a major opportunity for software organizations, but requires precise documentation to meet increased IRS scrutiny. BlueOptima’s CodeLedger provides a data-driven, automated solution that identifies CapEx and OpEx at a granular level, tracks location-based efforts, and delivers audit-ready documentation.